All Categories

Featured

Table of Contents

Trustees can be relative, relied on individuals, or financial organizations, depending upon your preferences and the intricacy of the count on. Ultimately, you'll require to. Properties can include money, property, supplies, or bonds. The objective is to ensure that the trust is well-funded to fulfill the youngster's long-lasting financial needs.

The role of a in a child assistance trust can not be underrated. The trustee is the individual or company accountable for managing the depend on's properties and guaranteeing that funds are distributed according to the terms of the trust contract. This includes making sure that funds are utilized only for the kid's benefit whether that's for education and learning, treatment, or everyday expenditures.

They must likewise provide regular records to the court, the custodial moms and dad, or both, depending on the terms of the trust. This accountability makes certain that the depend on is being handled in a means that benefits the child, protecting against abuse of the funds. The trustee also has a fiduciary responsibility, indicating they are legitimately obligated to act in the ideal interest of the child.

By buying an annuity, parents can make certain that a taken care of amount is paid frequently, despite any type of variations in their income. This offers comfort, recognizing that the youngster's needs will certainly remain to be fulfilled, despite the economic situations. Among the crucial advantages of making use of annuities for child assistance is that they can bypass the probate procedure.

How do I receive payments from an Secure Annuities?

Annuities can likewise use protection from market variations, ensuring that the child's financial backing continues to be stable also in unstable financial problems. Annuities for Youngster Support: An Organized Remedy When establishing, it's important to take into consideration the tax obligation effects for both the paying parent and the youngster. Trust funds, depending on their framework, can have various tax obligation treatments.

In other situations, the beneficiary the child might be accountable for paying taxes on any type of circulations they get. can also have tax obligation effects. While annuities give a stable income stream, it is very important to comprehend just how that income will certainly be exhausted. Depending on the structure of the annuity, payments to the custodial parent or child may be taken into consideration gross income.

Among one of the most significant benefits of using is the capability to safeguard a kid's financial future. Trust funds, specifically, supply a degree of defense from lenders and can ensure that funds are made use of sensibly. As an example, a trust fund can be structured to make certain that funds are only used for certain purposes, such as education and learning or health care, protecting against misuse - Flexible premium annuities.

What should I look for in an Annuity Withdrawal Options plan?

No, a Texas child support count on is especially made to cover the youngster's important needs, such as education, health care, and day-to-day living expenses. The trustee is lawfully bound to make sure that the funds are used only for the advantage of the kid as outlined in the trust agreement. An annuity gives structured, predictable settlements in time, making certain constant financial backing for the kid.

Yes, both kid support trusts and annuities featured prospective tax obligation implications. Trust income might be taxed, and annuity settlements can additionally be subject to taxes, relying on their structure. It's crucial to seek advice from with a tax obligation professional or financial consultant to recognize the tax duties connected with these monetary devices.

How do I receive payments from an Annuity Contracts?

Download this PDF - View all Publications The senior population is big, growing, and by some quotes, hold two-thirds of the specific riches in the United States. By the year 2050, the number of senior citizens is predicted to be virtually twice as huge as it was in 2012. Since numerous senior citizens have had the ability to conserve up a nest egg for their retired life years, they are frequently targeted with fraudulence in a means that more youthful people without any savings are not.

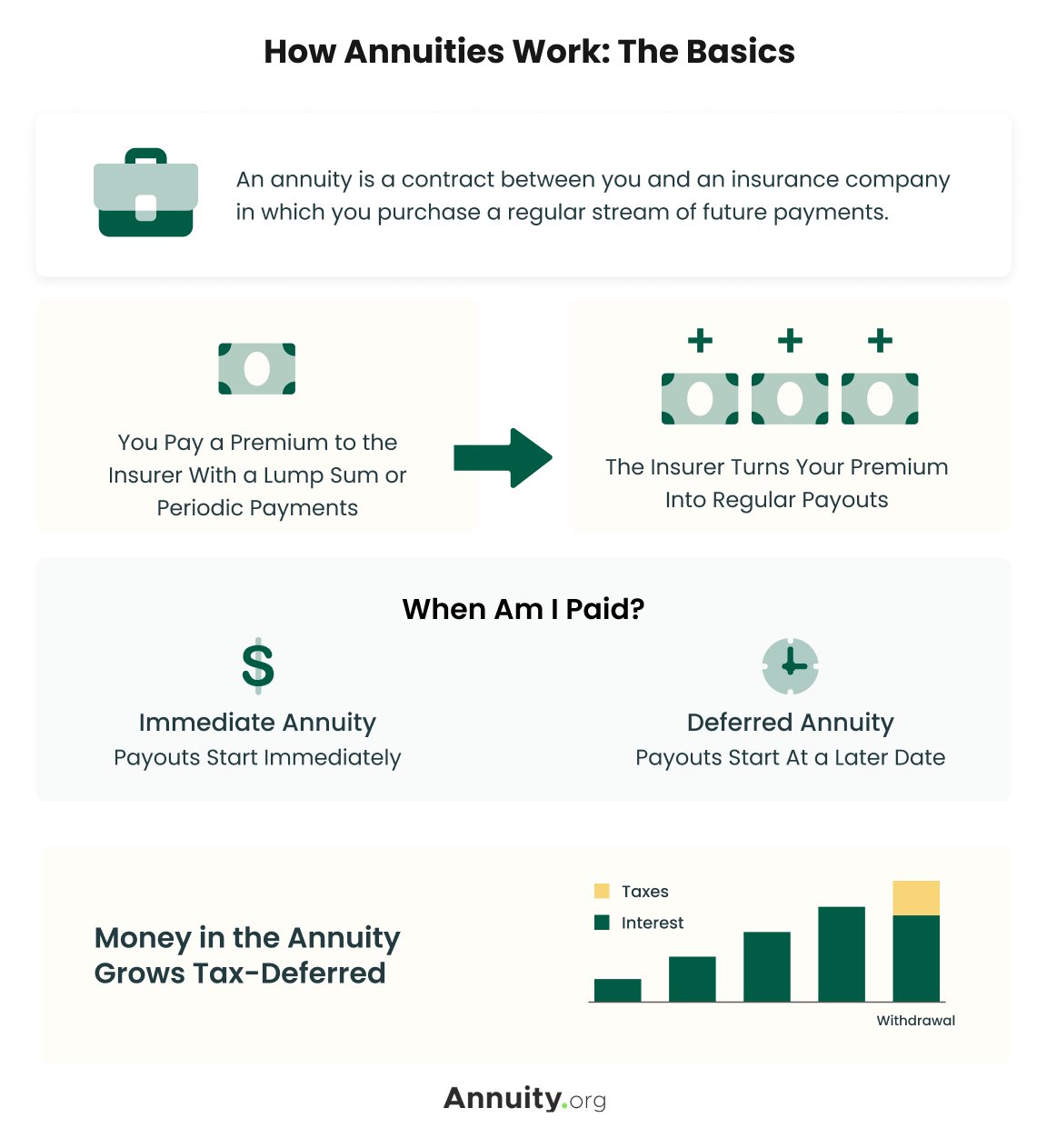

The Lawyer General gives the complying with ideas to consider prior to buying an annuity: Annuities are difficult investments. Annuities can be structured as variable annuities, fixed annuities, prompt annuities, deferred annuities, etc.

Customers need to read and comprehend the program, and the volatility of each financial investment provided in the syllabus. Financiers must ask their broker to explain all conditions in the syllabus, and ask questions about anything they do not recognize. Fixed annuity products might likewise bring threats, such as long-lasting deferment periods, barring investors from accessing every one of their cash.

The Attorney general of the United States has filed lawsuits against insurance provider that marketed unsuitable postponed annuities with over 15 year deferment periods to investors not expected to live that long, or that require access to their money for health care or helped living expenses (Income protection annuities). Capitalists should make certain they know the long-term effects of any kind of annuity acquisition

Annuity Withdrawal Options

Beware of seminars that offer free meals or gifts. Ultimately, they are seldom free. Be cautious of agents who provide themselves phony titles to enhance their integrity. The most significant cost connected with annuities is often the surrender fee. This is the percent that a consumer is billed if she or he takes out funds early.

Consumers might want to speak with a tax obligation specialist before investing in an annuity. Furthermore, the "safety and security" of the investment relies on the annuity. Beware of agents that aggressively market annuities as being as secure as or much better than CDs. The SEC advises customers that some vendors of annuities products urge consumers to switch to one more annuity, a method called "spinning." Regrettably, agents may not properly divulge costs connected with switching financial investments, such as new abandonment fees (which normally begin over from the day the item is changed), or substantially altered advantages.

Agents and insurer may use rewards to lure investors, such as extra passion points on their return. The benefits of such "bonuses" are usually surpassed by enhanced costs and management expenses to the capitalist. "Rewards" may be merely marketing tricks. Some deceitful representatives urge consumers to make impractical financial investments they can not pay for, or buy a long-lasting deferred annuity, also though they will require access to their cash for healthcare or living costs.

This area provides info beneficial to senior citizens and their households. There are several celebrations that may impact your advantages. Gives information often requested by brand-new senior citizens including changing health and wellness and life insurance policy choices, Sodas, annuity repayments, and taxable parts of annuity. Explains how advantages are impacted by occasions such as marriage, divorce, fatality of a spouse, re-employment in Federal service, or inability to handle one's funds.

What does an Deferred Annuities include?

Key Takeaways The recipient of an annuity is an individual or company the annuity's owner marks to get the contract's fatality benefit. Different annuities pay out to recipients in different ways. Some annuities may pay the recipient consistent repayments after the agreement holder's fatality, while other annuities might pay a survivor benefit as a lump amount.

{kind=link}

Table of Contents

Latest Posts

Analyzing Strategic Retirement Planning Everything You Need to Know About Variable Vs Fixed Annuities What Is the Best Retirement Option? Advantages and Disadvantages of Fixed Annuity Vs Variable Annu

Highlighting Fixed Vs Variable Annuity Pros Cons A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Vs Variable Annuity Pros and Cons of Fixed Vs Variable Annuity Why Choosi

Decoding How Investment Plans Work A Closer Look at Fixed Indexed Annuity Vs Market-variable Annuity Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Fixed Income A

More

Latest Posts